US banks pin hopes on digital to offset flagging GTB revenue

Hammered by low interest rates, transaction banking revenues at the top US banks fell to a three-and-a-half-year low. They’re now depending on treasury digital transformation and surging investment banking fees to offset the trend.

There is increasing evidence that treasury digital transformation can save millions of dollars from the corporate bottom line. Now, such transformation is becoming vital to the global transaction banks that provide treasury services as traditional corporate deposit-taking revenues come under pressure.

Consider how in the first quarter of 2021, US banks including Citigroup, Bank of America and JP Morgan reported a 10.8% fall in Global Transaction Banking (GTB) revenue from a year ago, taking the metric to a 14 quarter low of $6.045 billion. This fall was led by Bank of America as GTB revenues declined by 18% followed by Citigroup and JP Morgan reporting a fall of 10.6% and 4.8% respectively in the same time period.

In this quarter, JP Morgan overtook Citigroup as the highest transaction banking revenue generator amongst the three banks, as its revenue stood at $2.235 billion as compared to $2.165 billion at Citigroup.

![]()

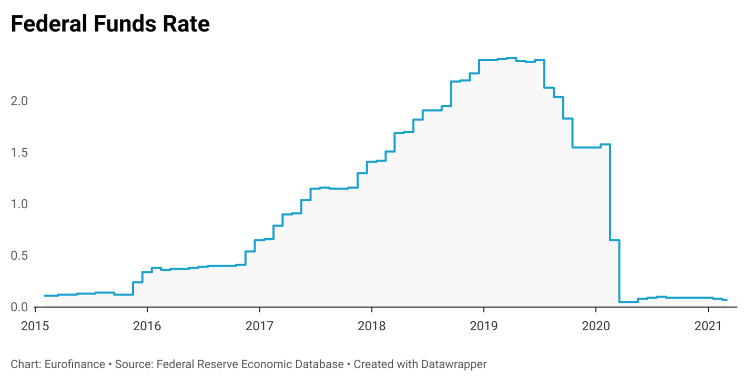

In the past, it was straightforward for the US giants to rely on their global scale and harvest as many corporate deposits as possible. They earned billions in revenues from the difference between the deposit rates paid to treasury clients, and the income from loans. Now, record low interest rates have compressed this differential, posing a challenge for the banks.

“The low rate environment that we’ve been in, is a very big driver in what we’ve seen in the aggregate TTS (Treasury and Trade Solutions) revenues” said Mark Mason, chief financial officer at Citigroup.

Deposit slowdown

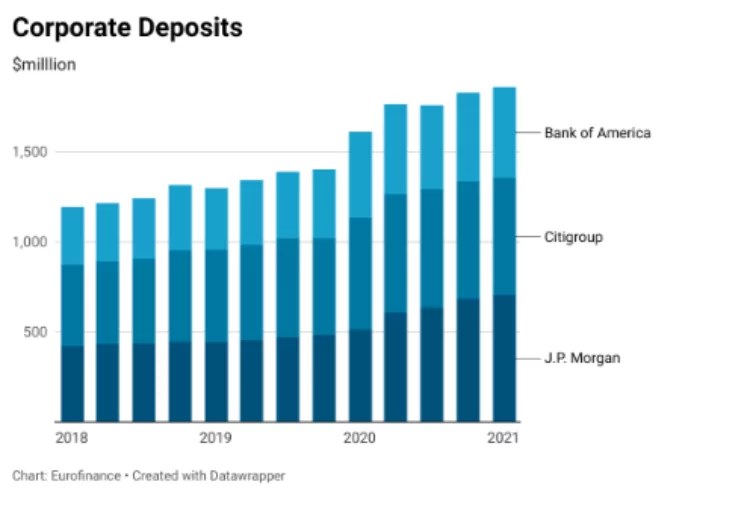

Due to the low rates offered on corporate deposits, treasurers are increasingly investing cash elsewhere, and this showed up as a slowdown in corporate deposit growth. In Q1 2021 JP Morgan and Bank of America’s deposit growth rates more than halved from the previous quarter, while Citigroup and Wells Fargo both reported corporate deposit declines.

By the end of the quarter, JP Morgan, Citigroup and Bank of America held corporate deposits of $705 billion, $649 billion and $505 billion respectively.

“It’s probably worth noting that the marginal benefit of further deposit growth is quite small given the fact that deployment opportunities are minimal” said Jennifer Piepszak, chief financial officer at JP Morgan.

Meanwhile, regulatory changes are making corporate deposits less attractive for large US banks. The Federal Reserve in March announced that it would end the temporary exclusion of bank Treasury bond holdings and central bank reserves from the Supplementary Leverage Ratio (SLR) calculation. This makes the banks less willing to accept additional corporate deposit liabilities.

“When a bank is leverage constrained, this lowers the marginal value of any deposit regardless if it is wholesale or retail, operational or non-operational and regulators should consider whether requiring banks to hold additional capital for further deposit growth is the right outcome”, JP Morgan’s Piepszak explained.

Focus on digital transformation

Given the consistent fall in GTB revenues since 2019 and how technology has evolved, big banks have shifted focus towards offering corporate treasurers a package of robust and innovative digital banking platforms.

As of February 2021, Bank of America has 74% active digital clients across corporate, commercial and business banking, which has increased by 3% over the past year. “Wholesale digital engagement continued to accelerate and usage continued to grow, driven by the same ease, safety, and convenience of our digital banking capabilities that our consumer customers enjoy.” said, Paul Donofrio, chief financial officer at Bank of America.

Citigroup’s efforts to digitally transform the transaction banking business are visible as client engagements with increased digital adoption and penetration have led to a rise in cross-border flows and clearing volumes by 7% and 6% respectively over the year. The company also appointed Tasnim Ghiawadwala as the Head of Citi Commercial Bank in April 2021 to drive growth along with the expansion of Citi’s digital platforms as a part of its overall transformational efforts.

“You’ll hear us also talk more about the commercial bank going forward as well, because the mid-market clients and the born digital clients are ones who use our TTS platform and the capabilities and services around it to also themselves start growing internationally and it becomes a core part of them.” said Jane Fraser, chief executive officer at Citigroup in a 15th April conference call.

Rise in Investment Banking

By contrast to transaction banking, investment banking units at the US banks provided relief to the top line by generating record revenues as corporates approached buoyant capital markets to raise funds. JP Morgan led the pack with a 57% growth in revenue on a year-on-year basis while Bank of America and Citigroup grew by 54.7% and 45.7% respectively in the same time period.

“IB fees of $3 billion were up 57% and while we now rank number 2 largely due to SPAC IPOs, we maintained our global IB wallet share of 9%. The quarter’s performance was an all-time record, driven by the continued momentum in the equity issuance markets as well as robust activity in M&A and DCM.” said Jennifer Piepszak, chief financial officer at JP Morgan on a 14th April conference call.