European corporates boost deposits by $100 bn in Q3 as they pivot from bank loans to capital markets

The top four European banks saw a surge in corporate deposits while at the same time experiencing a drop in outstanding loans for two straight quarters.

Unlike their US counterparts, European companies continued to build liquidity piles in the three months to 30 September, according to the analysis of disclosures by HSBC, Deutsche Bank, BNP Paribas and Barclays, most of whose exposures are in Europe. This hoarding of cash occurred while the corporates used capital markets to repay loan facilities drawn down at the height of the pandemic.

The trend was evident from top European carmakers’ Q2 disclosures –VW, BMW and Daimler pumped up their liquidity holdings by 50%, 24% and 6.5% in the first half of the year in view of Covid-19 uncertainty.

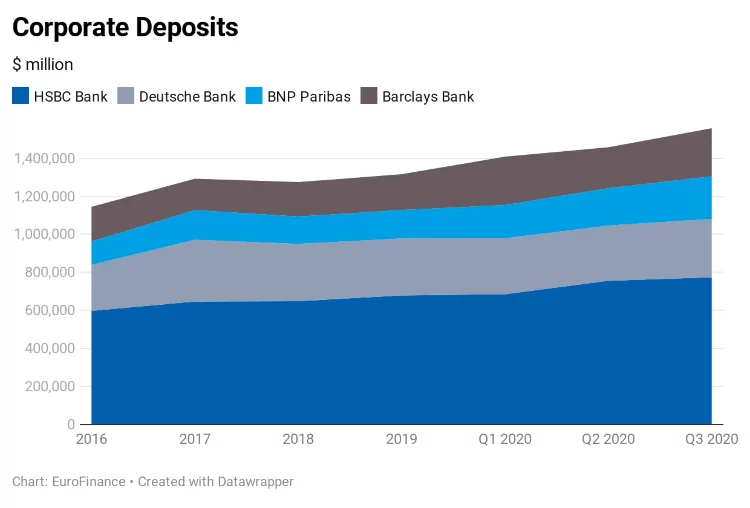

By the end of the third quarter, corporates had deposited $241 billion at – HSBC, Deutsche Bank, BNP Paribas and Barclays- representing a spike of 18% from the 2019 year end. These banks had a total of $1.55 trillion in corporate deposits of which $774 billion, $306 billion, $252 billion and $224 billion were held respectively. The largest spike was seen in BNP Paribas and Barclays by 50% and 34% in YTD terms.

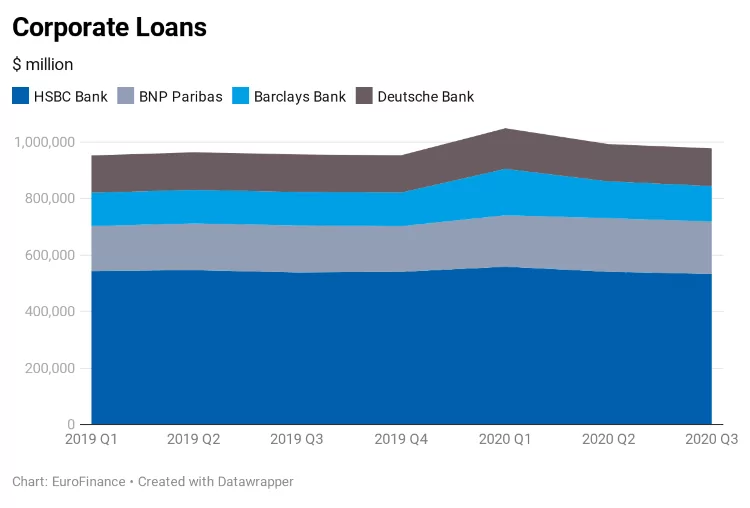

At the start of the pandemic in Q1, corporate clients of the four banks increased borrowing by $96 billion but since the end of Q1, they have reduced it by $71 billion, of which the large part of the reduction came in Q2 by $55 billion and by $15 billion in Q3.

At the end of Q3, total outstanding corporate loans at these banks were $977.4 billion. It had crossed a trillion dollar mark at end of Q1 2020. Barclays, BNP Paribas and Deutsche Bank do most of their corporate lending in Europe (including the UK). For HSBC it’s the second largest region after Asia-Pacific.

HSBC’s CFO Ewen James Stevenson in investors’ Q3 earnings call noted that “customer behaviour has been exactly what you would have expected it to be so far during the crisis” and he expected that consumers, as well as corporates, have “a desire to retain liquidity at the moment, given all of the uncertainty that exists”.

In the US, corporates in the third quarter have lowered their deposit as well as their outstanding loans at the top US banks namely J.P. Morgan, Wells Fargo, Citigroup and Bank of America. In the same period, corporates had reduced their outstanding loans by $166 billion.

In Europe, the trend is the opposite in the case of deposits. The corporates have up pumped their deposits but dropped their outstanding loans.

But HSBC’s CFO has commented on this in the Q3 earnings call that “assuming economies continue to rebound from COVID-19 lows, we would expect some increase in corporate investment and loan growth from the low levels seen in second and third quarters this year”.

As BNP Paribas’s CFO observed in Q3 earnings call that its Corporate and Institutional Banking division witnessed “a progressive shift from traditional bank lending, mostly in the form of syndicated loans to bond and also equity issuances with a view to strengthen the balance sheets of our (corporate) clients”.

While Deutsche Bank’s CEO Christian Sewing also pointed out that the drop in their loan books was due to “the issuances in the capital markets which were partially used to repay us”.

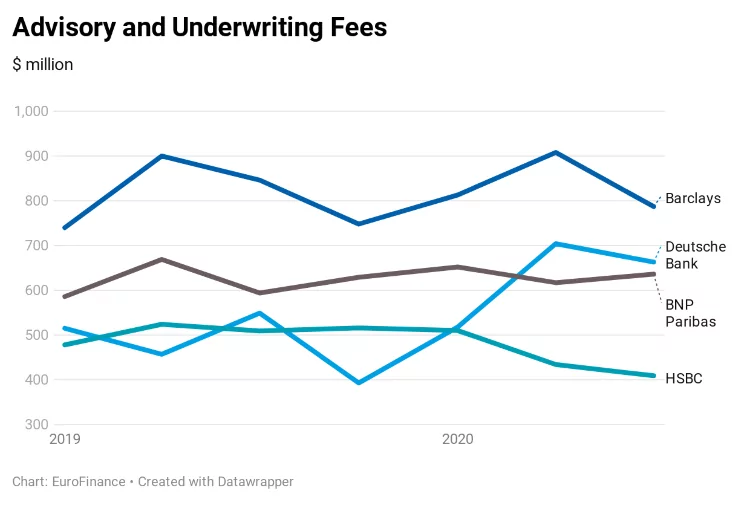

The advisory and underwriting fees at these banks saw a decline in third-quarter after a formidable growth first and second quarter this year.

At the end of Q3, nine months ending advisory and underwriting fees of Barclays, BNP Paribas, Deutsche Bank and HSBC stood at $2.5 billion, $1.9 billion, $1.88 billion and $1.35 billion respectively. Compared to the same period last year, Deutsche Bank saw a growth of 24% while HSBC saw a decline of 10%.

Non-financial corporation deposits as documented by the European Central Bank and Bank of England saw modest growth in Q3 as compared to the previous quarter. It grew by €100 billion in Q3 from Q2 while BoE said deposits grew by £19.6 billion in the same period.

At the end of Q3, corporate deposits tracked by the ECB crossed €3 trillion mark while at BoE, it stood at £536 billion.